Schwab’s reported prediction markets effort with Cboe will put prediction markets on the same screen as stocks, ETFs, and options. When the plan reaches customer accounts, the simplest prediction-market trade may become a brokerage-account action before crypto platforms can own the category.

A June 20 Wall Street Journal report said Schwab is collaborating with Cboe on products tied to whether the S&P 500 closes above or below specified levels. The report points to finance-related outcomes, including a Plus Zone-style feature.

Cboe has already shown how prediction-style exposure can fit inside the regulated options market. Its March framework described a Mini-SPX product using a traditional options wrapper, cash settlement, OCC clearing, and fixed-return outcomes.

Cboe’s later listing notice and June materials around Mini S&P 500 Index Binary Options show the idea reaching exchange infrastructure. The Mini-SPX binary options design sits in listed derivatives and borrows the retail-friendly part of crypto prediction markets: a simple answer to a simple outcome question.

How Cboe turns prediction-market odds into options

Prediction markets became easy to explain because the trade is straightforward. A user buys exposure to a yes-or-no outcome, the price implies a probability, and the payout depends on whether the event happens.

Crypto platforms such as Polymarket made that format legible to a mass audience around elections, sports, macro events, and crypto outcomes.

Cboe’s approach keeps the user-facing simplicity while changing the underlying machine. Its framework says the first product would be tied to Mini-SPX, use a traditional options wrapper, and settle in cash through the existing listed-options system.

A related Cboe binary options FAQ described XSP binary contracts with short-dated expirations, regular-hours trading at launch, and fixed outcome mechanics. A June fee filing added the kind of customer-fee detail that turns an idea into a broker-ready market structure.

However, the design is more conventional than a crypto market where users trade tokenized outcomes, but that is the point. The Cboe version reduces user friction by avoiding wallets, stablecoin balances, bridge risks, and market-resolution disputes.

It can sit where retail investors already keep cash, equities, ETFs, and options approval.

That notably changes the user journey. Cboe is recasting S&P 500 outcomes as a product inside a market retail investors already know.

For a Schwab customer, if the reported work reaches customer accounts, S&P 500 outcome trades could look like selecting another listed derivative from a familiar broker screen.

Cboe’s broader binary-options proposal also sits apart from a completed Schwab rollout. The Federal Register notice shows regulators extended action on a broader Cboe proposal into July 2026.

The timing is not linked. Cboe’s materials show product infrastructure across the June listing, FAQ, and fee documents, while customer-facing availability with Schwab remains unconfirmed as of press time.

Why brokerage screens are the prediction-market battleground

Schwab will enter a market already moving toward brokerage screens. Robinhood has added prediction-market access to its app via Robinhood Derivatives and Kalshi, while Interactive Brokers offers event-contract access from a single IBKR account alongside other assets.

CryptoSlate has also previously covered how prediction markets were moving toward brokerage accounts before the Schwab/Cboe report.

That context frames Schwab as part of a distribution contest rather than a first mover. Schwab has a large, trust-heavy retail base. Cboe has listed-derivatives infrastructure.

Put the two together, and the easiest piece of the prediction-market pitch, a trade with a defined outcome and a fixed payout, can be delivered without asking users to leave the brokerage environment.

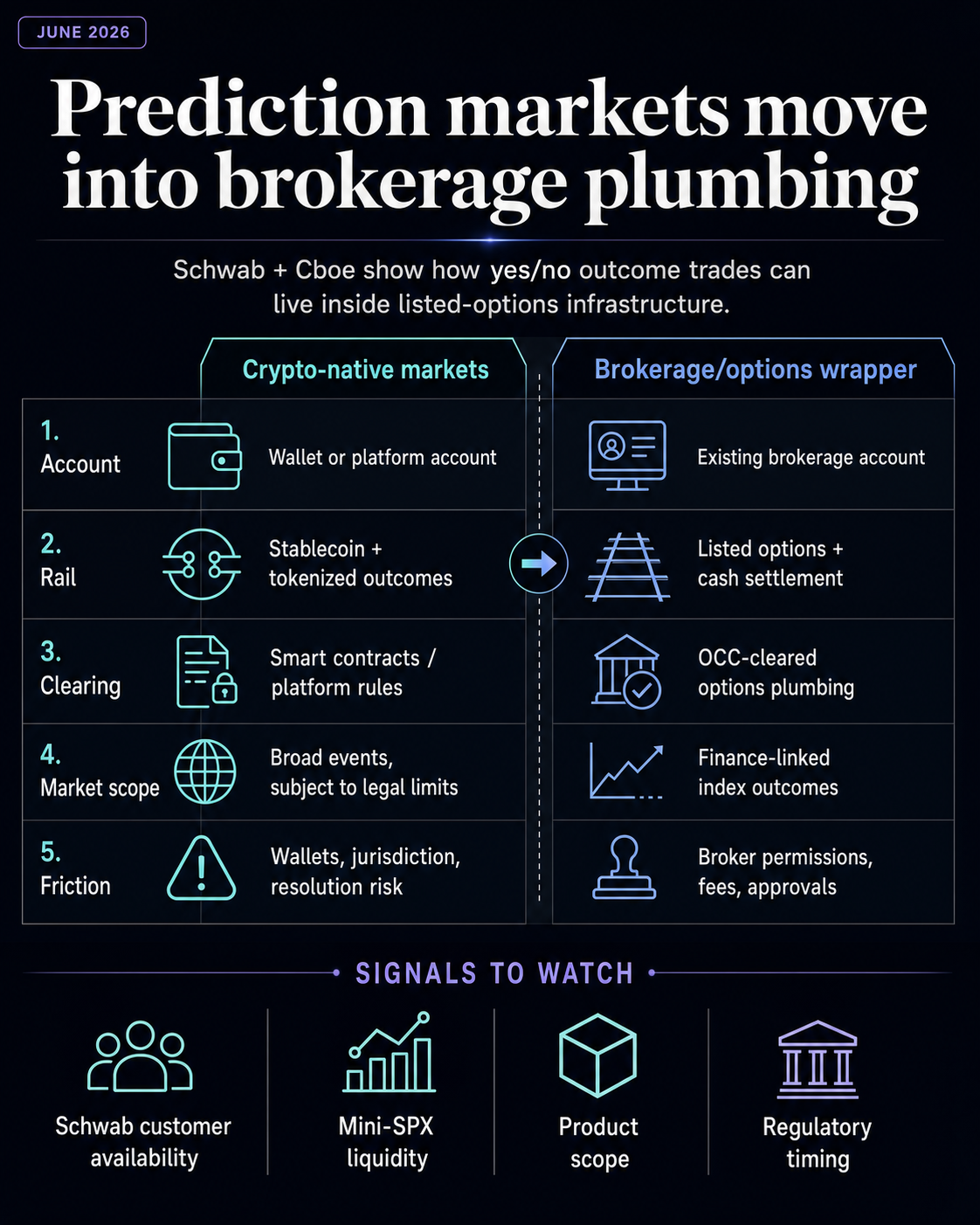

| Feature | Crypto-native prediction market | Brokerage/options-based outcome contract |

|---|---|---|

| Account | Wallet or platform account connected to crypto rails | Brokerage account with existing cash and options workflows |

| Rail | Stablecoin, tokenized outcomes, and crypto settlement infrastructure | Listed options, cash settlement, and clearinghouse plumbing |

| Payout feel | Yes-or-no or outcome-token exposure | Fixed-return binary or prediction-style options exposure |

| Market scope | Broad event categories, subject to platform and legal constraints | Finance-linked contracts where exchange and broker approval fit |

| Main friction | Wallet setup, jurisdiction limits, liquidity trust, and resolution risk | Broker permissions, regulatory approvals, fees, and product scope |

The table above shows why the brokerage version can be powerful even with a smaller event menu. Its power comes from making the clearest retail use case feel safer, cleaner, and closer to the investor’s existing money.

What remains crypto-native is the part brokers are least likely to absorb. For example, Polymarket’s documentation uses a different stack: pUSD collateral, tokenized Yes and No shares, peer-to-peer central-limit-order-book trading, wallet-based access patterns, and resolution infrastructure tied to crypto-native market design.

Still, that stack holds its value. It can support markets that do not fit neatly into a listed-options wrapper. It can move faster around culturally live events.

It can connect users globally, subject to legal and platform constraints, without relying on a single broker’s product menu. Those strengths explain why crypto-native prediction markets became a meaningful category before brokerage distribution caught up.

Schwab and Cboe could take share from that model without copying it. They could leave sports, culture, politics, and long-tail events to other venues while taking the cleanest financial-outcome use case: major index levels, short-dated market views, and contracts that look closer to retail options than to internet betting markets.

CryptoSlate’s recent coverage of Kalshi, sportsbooks, and crypto rails shows that the broader prediction-market fight is still playing out across legal, exchange, and platform boundaries. The Schwab/Cboe lane is more specific: financial outcomes routed through regulated brokerage plumbing.

What changes if Schwab follows through

The near-term consequence is that the category’s easiest explanation may shift away from crypto as an advantage. If a mainstream investor can express a view on the S&P 500 close through a broker, the user-education problem changes.

The main choice becomes which venue gives the best mix of trust, liquidity, scope, price, and access.

One path is that Schwab and Cboe make financial outcome contracts feel like another retail derivatives feature.

Crypto-native markets would still keep broader event coverage and faster experimentation, but the most approachable product format would become shared territory. Another path is more contained: regulatory timing, product limits, fees, or broker caution leave the listed-options version with a smaller footprint, giving crypto-native and event-contract platforms more room to define the category.

The signals to watch are concrete. Schwab would need to confirm customer availability, scope, and product mechanics.

Cboe’s filings and notices would need to show how Mini-SPX binary options actually trade, what fees look like in practice, and whether liquidity develops beyond launch materials. Regulators will continue to shape the boundary between listed financial contracts and broader event markets.

For crypto, the lesson is already visible. Prediction markets may have been popularized by crypto-native venues, but the simplest mechanic is portable.

If Wall Street can put that mechanic inside the broker account, crypto’s defensible edge has to be the part brokers cannot easily absorb: market breadth, settlement design, global participation patterns, and the ability to build around events faster than regulated product cycles move.