Arthur Hayes outlined a path to $1 million Bitcoin price built around AI absorbing liquidity, the buildout collapsing under debt, authorities printing, and capital rotating into crypto.

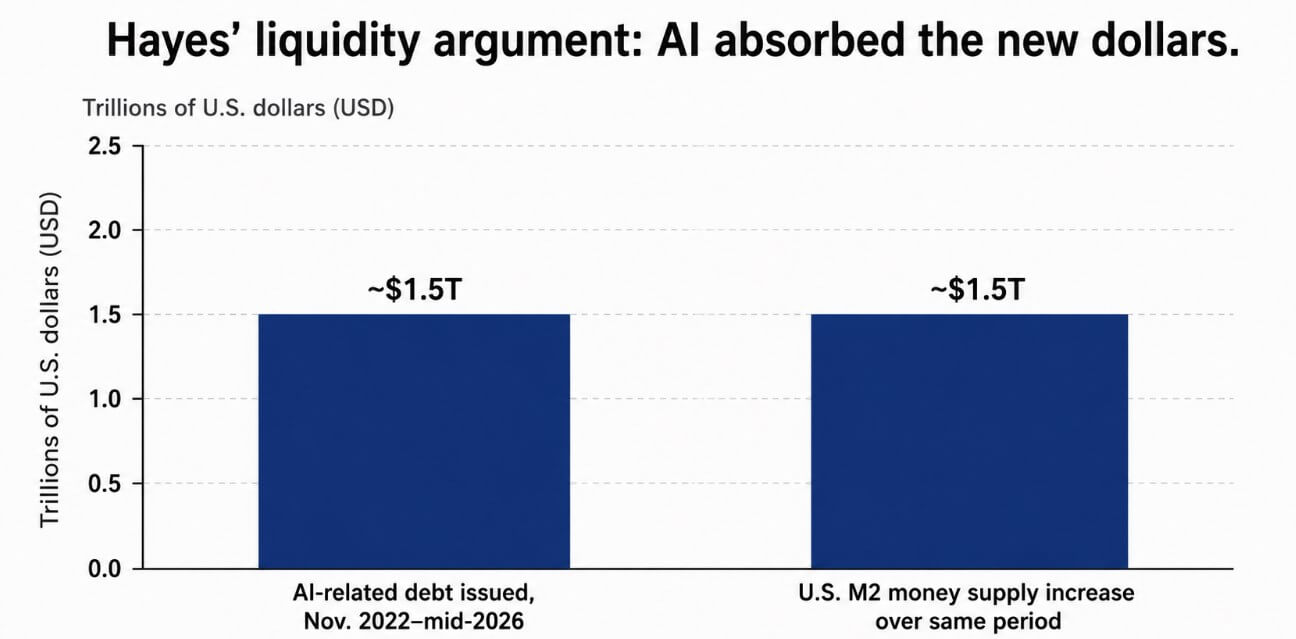

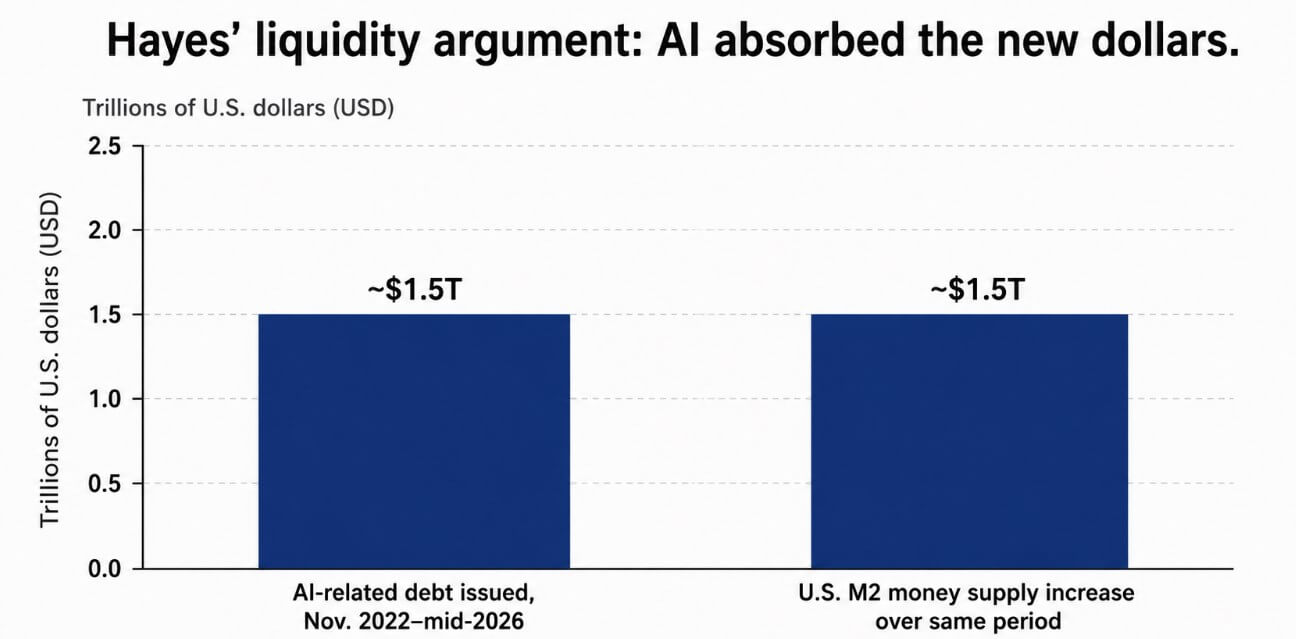

Hayes made the argument on Bankless, saying that AI became the dominant capital sink, and his Substack essay noted that roughly $1.5 trillion in AI-related debt was issued between November 2022 and mid-2026.

The amount nearly matches the $1.5 trillion rise in the M2 money supply over the same period, with newly created dollars absorbed by data centers and GPU clusters before reaching Bitcoin’s bid.

Luke Gromen, founder of Forest for the Trees, arrived at the same diagnosis from a different entry point. Speaking on the Coin Stories podcast in June, he described the current market structure as unhealthy beneath record equity indices, with AI-related names concentrating the gains while breadth deteriorated.

Gromen said:

“AI is sucking all the oxygen out of the room, all the liquidity out of the room, and I think that’s happening to Bitcoin as well.”

He called Bitcoin “one of, if not the last functioning smoke alarm of liquidity,” a signal asset that warns investors about the broader liquidity picture before other markets confirm it.

Gromen sold most of his Bitcoin position near the top and has only nibbled back in, a stance consistent with Hayes’ near-term bearishness on crypto.

He extends the argument to AI infrastructure accounting, where companies book revenue upfront while spreading construction costs over time, inflating reported earnings and masking the moment when a buildout slowdown forces a sharp deceleration in cash flows.

Serious macro institutions are also worried about Bitcoin price

Apollo’s chief economist Torsten Slok wrote that the top 10 companies in the S&P 500 are more overvalued than the top 10 were during the 1990s tech bubble.

Those 10 names now represent roughly 40% of the index, meaning that $100 invested in the S&P 500 is a bet that the AI story will continue. A broad correction in that group spreads to every passive portfolio worldwide.

The Bank for International Settlements published a 2026 bulletin documenting what Hayes describes, with central bank credibility behind the warning. The BIS found that AI infrastructure investment is moving from internal cash flows to external debt as the scale of required investment overwhelms hyperscalers’ free cash flow.

Private credit outstanding to AI-related companies had grown from near zero to over $200 billion, with that share of total private credit climbing from below 1% to almost 8%.

The BIS flagged credit-standard and financial stability risks when expected returns fall short, and found that hyperscalers are also moving AI infrastructure debt off their balance sheets through special-purpose vehicles and operating leases, which the BIS calls “shadow borrowing.”

These moves strengthen links between tech companies and non-bank investors, creating new channels for the transmission of shocks if sentiment reverses.

Once AI infrastructure carries more than $200 billion in private credit with five-to-seven-year maturities, an AI slowdown becomes a credit-market risk rather than a narrow tech-sector problem.

| Risk layer | Evidence in the article | Why it matters for Bitcoin price thesis |

|---|---|---|

| Liquidity drain | Hayes and Gromen argue AI absorbed capital that might otherwise have supported Bitcoin price | Explains why BTC can lag despite money supply expansion |

| Equity concentration | Apollo says the top 10 S&P 500 names are more overvalued than during the 1990s tech bubble | A correction in AI-heavy mega caps would hit passive portfolios globally |

| Debt-funded buildout | BIS says AI infrastructure financing is shifting from internal cash flow to external debt | Turns AI from a tech-stock story into a credit-market story |

| Private credit exposure | BIS says AI-related private credit has grown from near zero to more than $200B | Creates non-bank transmission channels if AI returns disappoint |

| Shadow borrowing | BIS flags SPVs and operating leases used to finance infrastructure off balance sheet | Makes the true leverage behind AI harder to see |

| Policy response | Hayes argues a collapse would force authorities to print | Bitcoin price upside depends on whether rescue liquidity seeks scarce assets |

Where macro voices diverge

Lyn Alden’s framework provides Hayes with the financial backdrop and stops at a far less dramatic conclusion.

In her February and March newsletters, Alden described the Fed as entering what she calls a “gradual print,” consisting of balance sheet expansion aligned with nominal GDP growth, running between $220 billion and $375 billion in 2026, far below the scale of any prior crisis QE.

Her threshold for calling it a genuinely big print is $2 trillion or more. Hayes is describing a future crisis response that would clear that bar, while Alden is describing the current base case, which lands around $300 billion.

Bitwise’s 2026 advisor survey found that out of 299 financial advisors surveyed, 32% allocated to crypto in client accounts in 2025, the highest rate in the survey’s eight-year history.

Among those tracking crypto themes, “digital gold” and fiat debasement ranked second at 22%, behind stablecoins and tokenization at 30%. The debasement narrative is already distributed through ETFs and embedded in professional portfolios.

If the Fed response becomes the market story, Bitcoin already has the institutional argument preloaded inside existing allocations.

The sequence problem

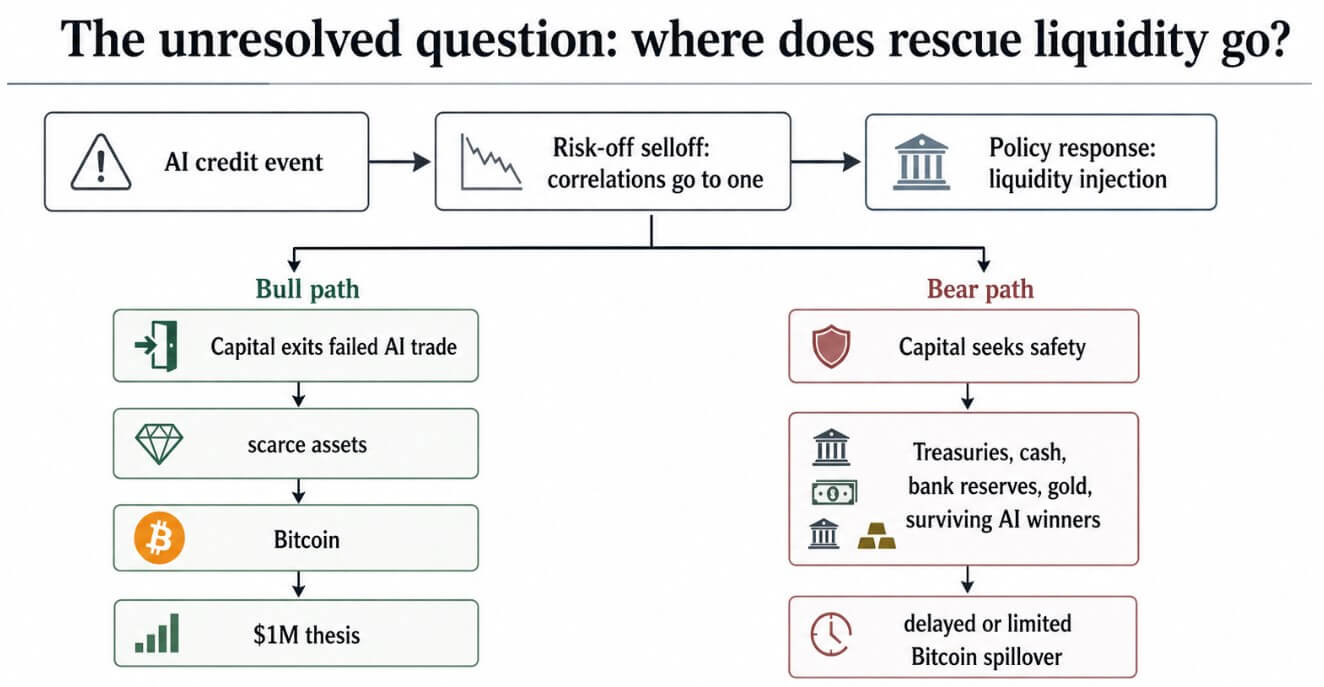

Hayes acknowledged on Bankless that in a broad risk-off event, correlations compress toward one and investors sell everything.

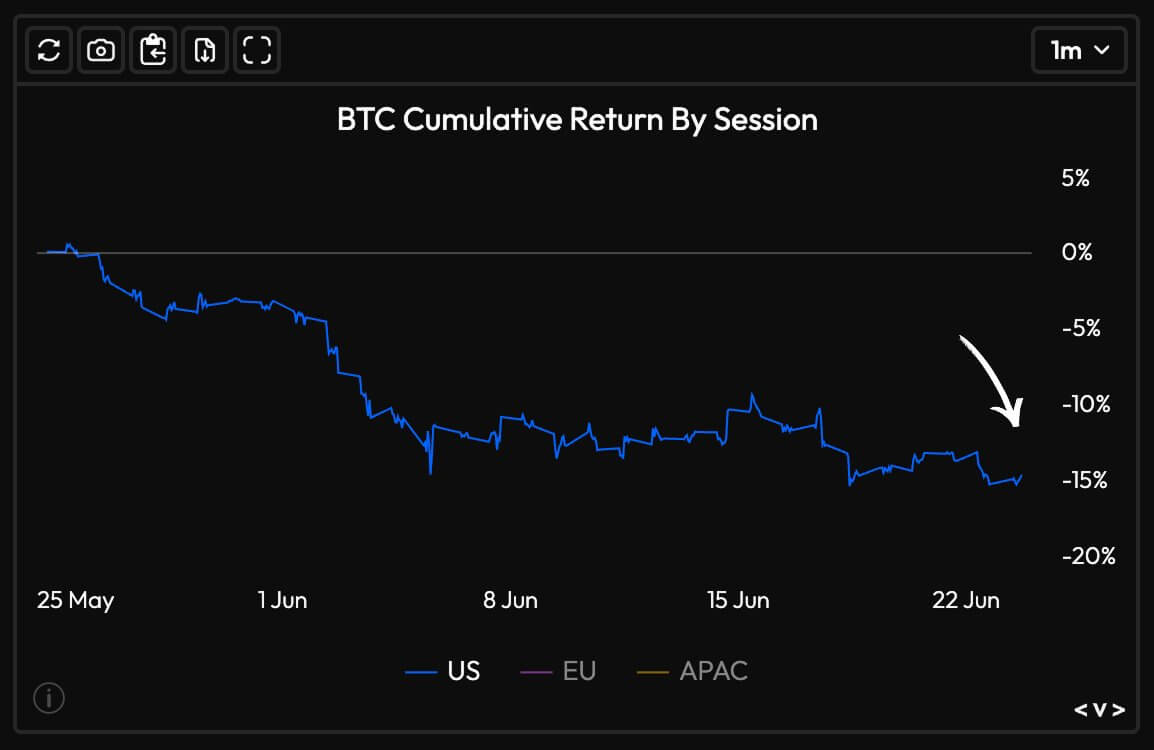

Bitcoin price fell roughly 50% from its October 2025 peak at $126,000, even as the money supply expanded.

An AI credit event would produce the same first-phase response: Bitcoin sells with risk assets, banks pull back on lending, and liquidity tightens before policymakers respond.

Hayes’ actual trade is the policy response that follows a crash, and whether investors who watched AI destroy capital would put freshly printed money back into the same sector.

The liquidity-drain analysis, the BIS debt data, and the Apollo valuation warnings document the setup. Capital destination is a decision made within the crisis itself, and those sources stop at its edge.

Two ways the money moves to affect Bitcoin price

The bull case depends on Hayes’ full sequence arriving intact. AI financing stress hits banks and private credit, policymakers inject major liquidity, and investors who watched $1.5 trillion in AI debt destroy value seek scarce assets detached from the failed trade.

Bitcoin price at $1 million per coin implies a fully diluted network value of roughly $21 trillion, a figure that would require crypto-native capital and a major reallocation of global macro portfolios.

Alden’s gradual-print environment provides the directional support; only Hayes’ crisis-scale injection produces the magnitude.

The bear case is that emergency liquidity flows first toward the safest collateral, such as Treasuries, cash, bank reserves, and gold. Surviving AI winners attract capital from investors seeking the sector’s strongest projects, keeping money within tech.

Bitcoin’s correlation with risk assets during the early phase of a credit event runs counter to Hayes’ destination, and the rescue money could remain in Treasuries, gold, and bank reserves for months before reaching crypto.

Hayes’ setup of AI debt, valuation excess, and liquidity distortion may prove entirely accurate. His destination is the part that depends on investor behavior inside a crisis, and that part is still open.