Venus Protocol has turned the use of tokenized stocks as DeFi collateral into a 2026 BNB Chain test by adding bStocks markets to its Core Pool, creating a way to assess lending risk controls before active borrowing becomes the main story.

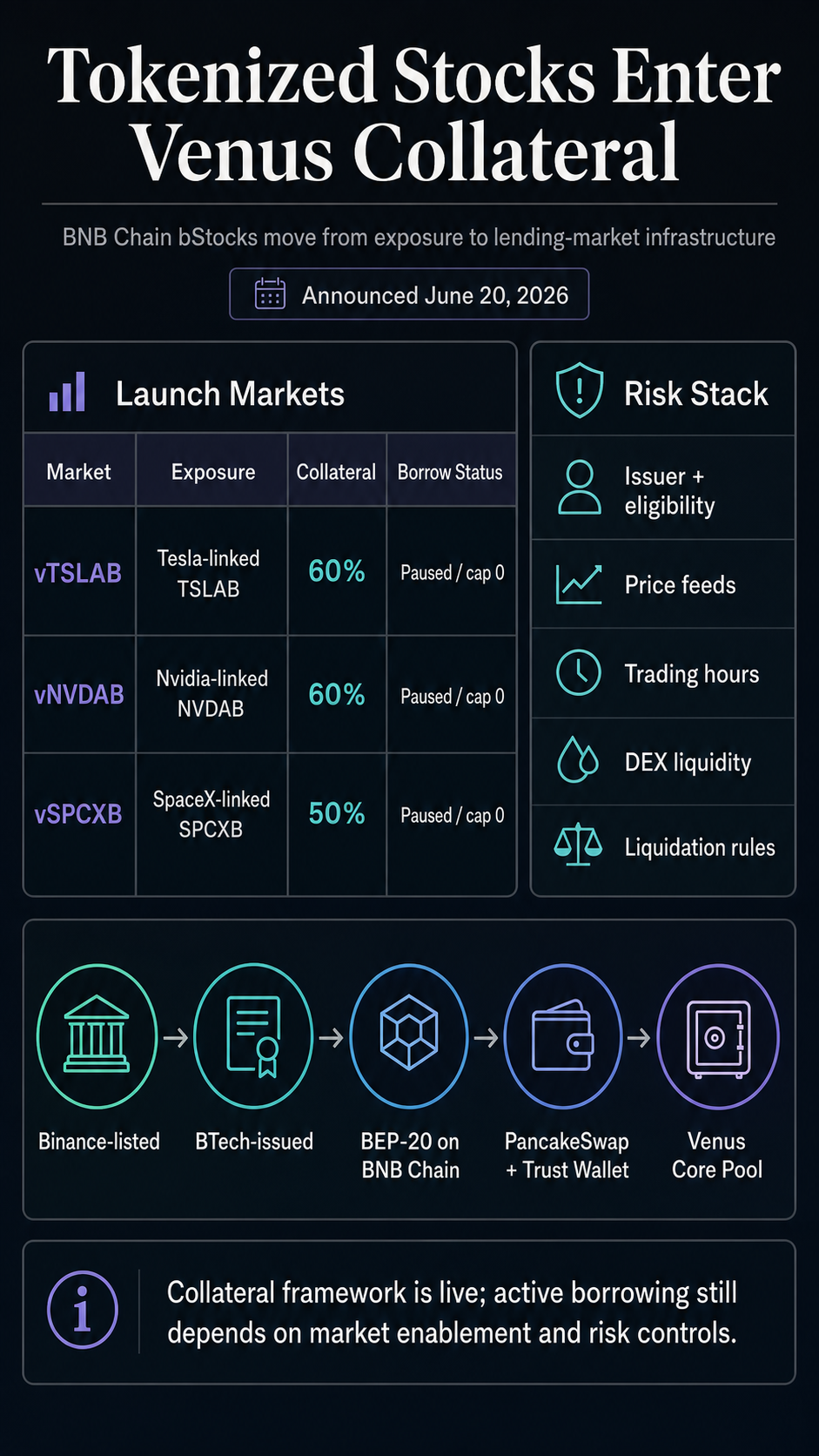

The June 20 rollout covers bStocks tied to Tesla, Nvidia, and SpaceX exposure: TSLAB, NVDAB, and SPCXB. The change gives eligible users a way to supply stock-linked assets into bStocks collateral markets inside Venus’ lending framework while keeping active stablecoin borrowing outside the verified launch claim.

Guardrails create market parameters that list collateral factors and caps and show borrowing paused, with borrow caps set to 0 at launch.

Venus has opened the collateral framework first, with real borrowing demand, stablecoin use, and liquidation behavior still to be proven after launch.

The risk profile differs from that of a normal token listing. Tokenized stock collateral depends on an issuer, permitted jurisdictions, market access, off-hours pricing, oracle design, collateral factors, supply caps, and liquidation rules.

Venus is testing whether equity-linked tokens can serve as productive collateral in a crypto money market before the regulatory and market structures around tokenized equities have settled.

Venus starts with tokenized stocks as DeFi collateral before open borrowing

The initial assets are high-profile enough to attract attention, but the risk parameters convey a stronger signal. Venus’ proposal lists TSLAB and NVDAB with 60% collateral factors and SPCXB with a 50% collateral factor, alongside caps and an oracle-protection trigger.

Those numbers show that the markets were designed as controlled exposure rather than an open-ended invitation to borrow immediately against tokenized equities.

| Venus market | Stock-linked exposure | Collateral factor | Launch borrow status |

|---|---|---|---|

| vTSLAB | Tesla-linked TSLAB | 60% | Borrowing paused / borrow cap 0 in proposal |

| vNVDAB | Nvidia-linked NVDAB | 60% | Borrowing paused / borrow cap 0 in proposal |

| vSPCXB | SpaceX-linked SPCXB | 50% | Borrowing paused / borrow cap 0 in proposal |

Venus has created a place where these assets can serve as collateral, while the verified launch record supports caution regarding claims that users are already borrowing USDT or USDC against the bStocks markets.

Stablecoins remain the likely practical borrow asset category because they are the main liquidity rail in DeFi.

The staged design gives Venus room to observe the assets before borrow demand arrives. A collateral market needs sufficient supply, reliable pricing, and predictable liquidation paths before debt can be safely built on top of it.

That work is harder when the collateral references equity exposure rather than a token that trades natively across crypto venues.

DeFi collateral markets usually begin with crypto-native assets or stablecoins because those markets trade continuously and have deep on-chain liquidity.

Tokenized stocks introduce a different set of timing and issuer dependencies. A position linked to a U.S. equity can be represented on-chain around the clock, while the underlying equity market, issuer permissions, and price feeds may behave differently than those of a 24/7 crypto asset.

The collateral framework has to account for that mismatch before the product can be treated like another liquid token.

Issuer rules now sit inside the lending stack

The assets Venus is adding are separate from ordinary shares. Binance describes bStocks as 1:1-backed tokenized securities available to eligible users in permitted jurisdictions, and the Binance product materials identify BTech Holdings Limited as the issuer.

Users should treat the tokens as stock-linked exposure rather than direct ownership of Tesla, Nvidia, or SpaceX shares. The product structure, eligibility rules, and issuer controls remain part of the asset’s risk profile.

Binance separately listed TSLAB and NVDAB spot pairs on June 11 and added SPCXB shortly afterward, creating the exchange access layer before Venus added the collateral-market layer.

BNB Chain then framed bStocks as BEP-20 tokenized U.S. securities that could be deployed across DeFi protocols, explicitly naming Venus among the integrations in its bStocks launch post.

The distribution path also has practical weight. PancakeSwap provides a decentralized trading route for bStocks, while Trust Wallet offers wallet access.

Together, those integrations help move the tokens from centralized listing venues into self-custody and DeFi interfaces. Access through a wallet or DEX still leaves the underlying eligibility, issuer, and market-structure constraints attached to stock-linked tokens.

The lending test will be whether those rails can support a market in which the benefits of new collateral outweigh the added constraints. A collateral market needs reliable pricing, predictable liquidation paths, enough liquidity to sell collateral when needed, and a clear understanding of who can hold or redeem the underlying product.

Those conditions are easier to satisfy for BTC, ETH, BNB, or major stablecoins than for a token tied to an equity product, which is subject to jurisdictional and issuer-level limits.

That makes the BNB Chain distribution more than just a reach metric. If bStocks can move between exchange access, wallets, DEX liquidity, and lending interfaces while keeping eligibility and risk controls intact, they become a more serious test of tokenized equity composability.

If any one of those layers breaks down, the market may remain a collateral listing with limited debt activity.

The test shifts from access to utility

CryptoSlate has tracked the broader push to bring tokenized equities and real-world assets into DeFi, including xStocks’ BNB Chain expansion and the gap between tokenized asset issuance and genuine DeFi composability.

Venus’ launch fits that broader pattern because it gives tokenized stocks a more demanding job than sitting in a wallet or trading on a DEX. That makes the launch an early test of real-world asset collateral in a live crypto money market.

The timing also puts Venus in the middle of an unsettled regulatory conversation, as recent CryptoSlate coverage has noted that tokenization leaves securities treatment unresolved.

For tokenized equity lending, that creates a two-part test. Protocols focus on liquidation mechanics, while regulators and issuers focus on who can access the instrument and what rights the token represents.

Market context gives the experiment some weight. CryptoSlate’s Venus page showed roughly $1.04 billion in TVL, while BNB remains one of the largest chain assets by market value.

Tether’s USDT and USD Coin remain core liquidity rails across crypto markets. The bStocks launch is early rather than systemically important on day one, but it places the test within a venue and chain ecosystem large enough for the outcome to count if supply and borrowing develop later.

The next signals are straightforward. First, whether Venus enables borrowing against these specific markets and which assets become available. Second, whether collateral supply arrives without relying mainly on incentives.

Third, whether price feeds and liquidation rules hold up when crypto trades continuously but equity-linked exposure depends on off-chain market structure. Finally, whether Venus expands beyond TSLAB, NVDAB, and SPCXB while keeping similar caps and protections.

The sourced record shows an early, revealing stage: Venus has built the first layer of a collateral market for stock-linked tokens, and the initial guardrails show how much must work before that exposure can function as productive DeFi collateral.